'/%3e%3c/svg%3e)

'/%3e%3c/svg%3e)

Finding the Best Options Strategy in 2026 – a Quant’s Data-Driven Approach

The best options strategy depends on your market view and preferences. OptiStrat algorithmically finds the ones that suit your constraints and objective from millions of live alternatives.

The Single Best Option Strategy to Trade

You came here to learn about the best options strategy, so let me be straight with you. No matter what the self-declared finance guru that sold you an overpriced slide deck in the shape of an educational course claims in his get-rich-quick scheme, the single best options strategy does not exist.

The answer depends on personal beliefs on the future market development, and constraints imposed by one’s personal risk tolerance. The different characteristics of an options strategy are inherently competing with one another. An incremental increase in exposure to the underlying’s price comes with less leverage; an improved time-decay schedule might reduce the potential for high payouts; and so on.

Suppose we expect Tesla (TSLA) stock to rise by 8% from $400 to $432 over the next 45 days with volatility unchanged. We could simply buy a Call option to gain decent exposure to moves in the underlying stock. However, this is likely to result in an inefficient trade since we are paying the full premium and suffer the entire time decay. An alternative strategy would be a Bull Call Spread, in which we buy a Call option below our target price and sell a Call option just above it at $435. This offsets part of the cost, time decay and many other factors, but also leaves us with less exposure to the stock’s moves.

Despite the reduced exposure to the underlying, such a Bull Call Spread structure is already likely to be superior to an outright single long Call in many cases. But this is far from the only option (pun intended). Short Put, Call Ratio Spread, you name it. Which options strategy is best depends on how one wants to weight these different dimensions and changes with every second and updated quote.

So, while suggesting a generic single best option is not possible, the OptiStrat feature on the OptiView platform evaluates all possible combinations for you automatically and in real-time. It finds the strategies that are best in the relevant dimensions. You can try it yourself on our platform.

An Algorithm to Optimize Your Option Strategy

In practice, finding optimal trades was the exclusive business of quant hedge-funds with sophisticated tools doing the work. Not so any longer. We released OptiStrat as an institutional-grade tool on the OptiView platform that has access to live quotes and compares all possible strategies algorithmically to find the setup that offers the most cost-efficient way to position according to your constraints and objectives.

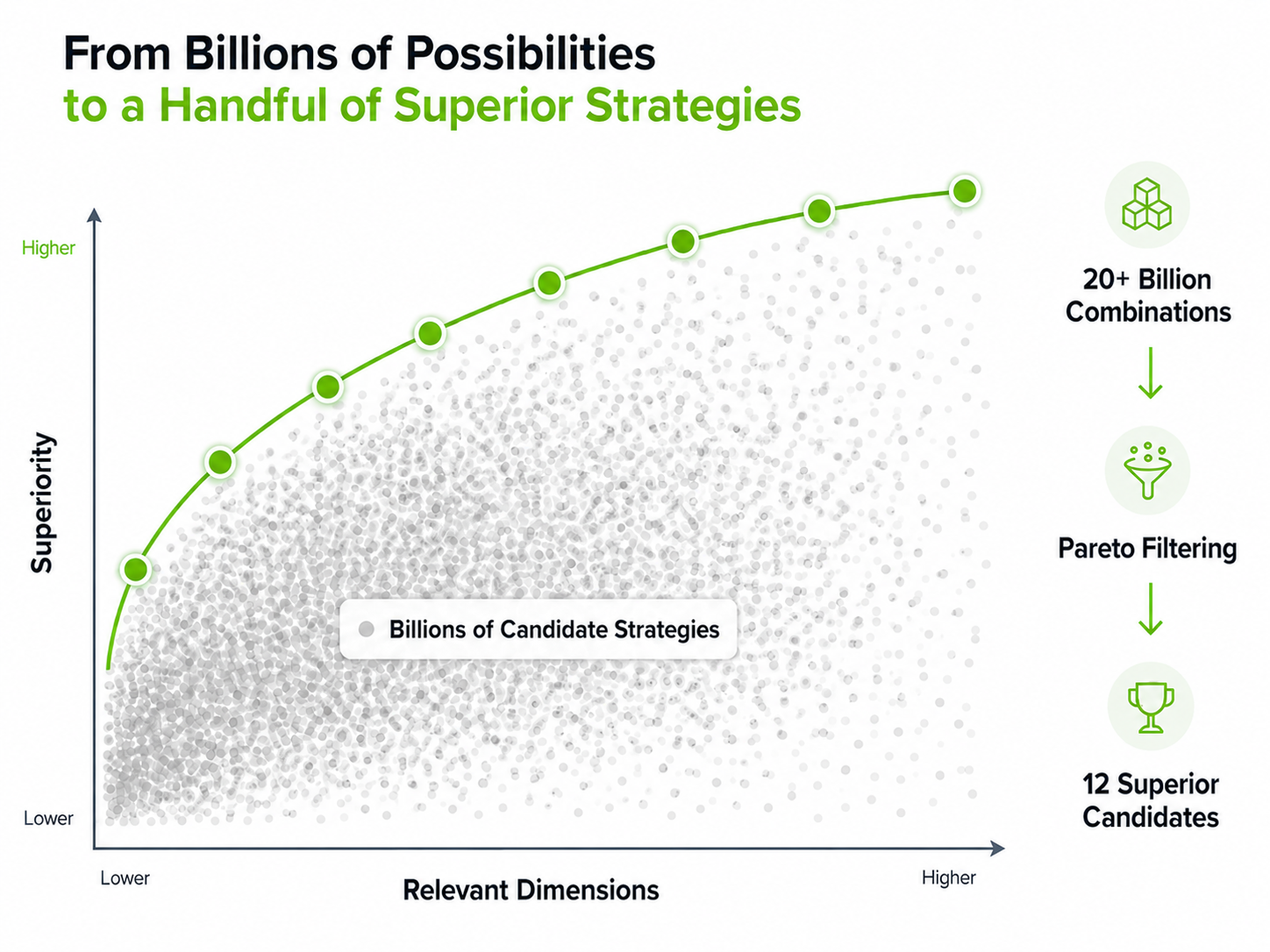

Under the hood, it constructs a subset of superior combinations that are strictly better than all alternatives in the dimensions that matter.

The most relevant dimensions when assessing an options strategy are:

- the gained exposure to the underlying;

- the duration over which the exposure is maintained;

- the leverage amplifying gains or losses;

- and obviously, risk-adjusted return itself.

The result is a Pareto-efficient frontier of superior strategies along the dimensions that matter when investing with options. A strategy is Pareto-efficient if no alternative is better in all dimensions. Depending on the desired exposure, this often reduces the set of potential alternatives from millions down to just a handful.

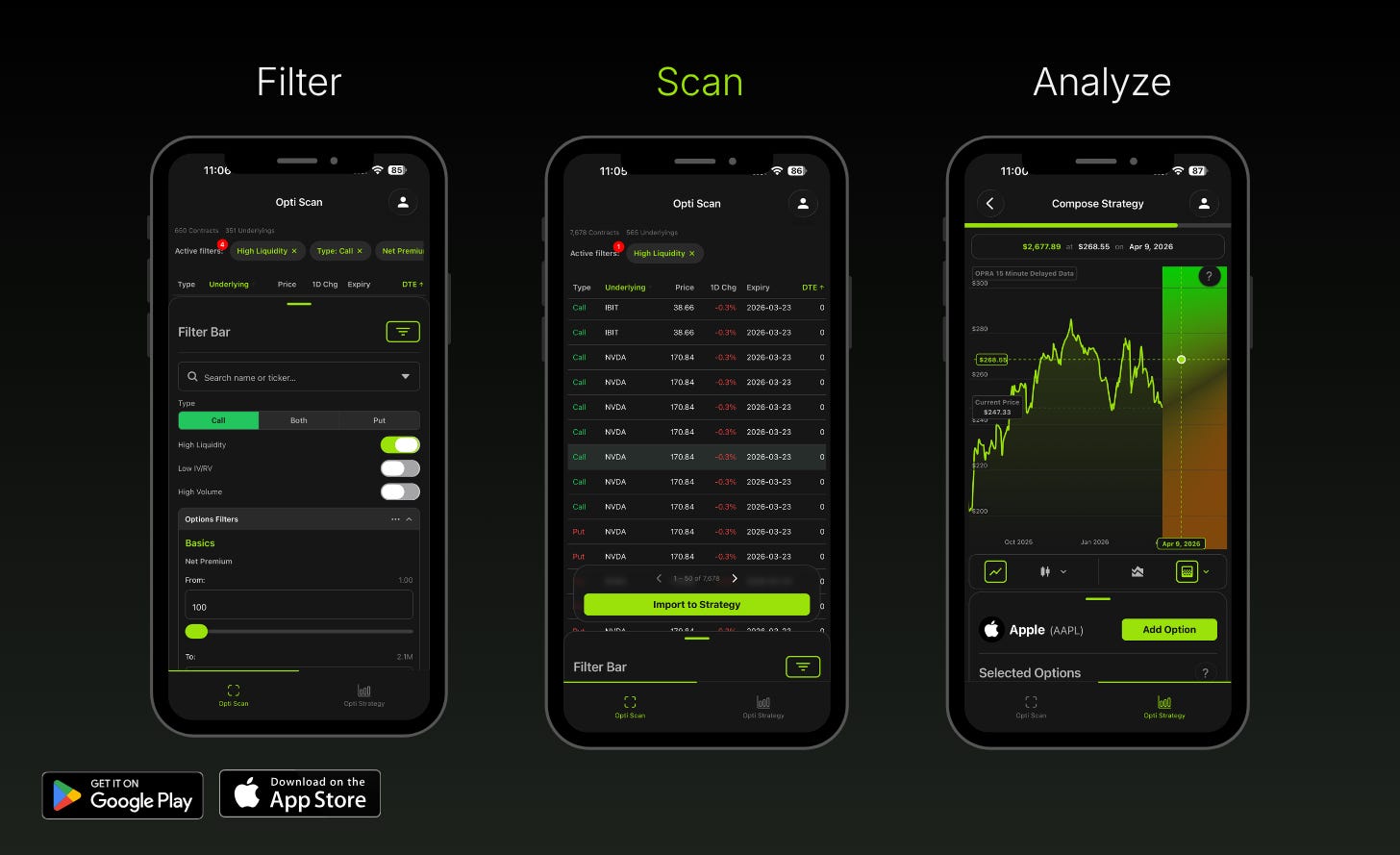

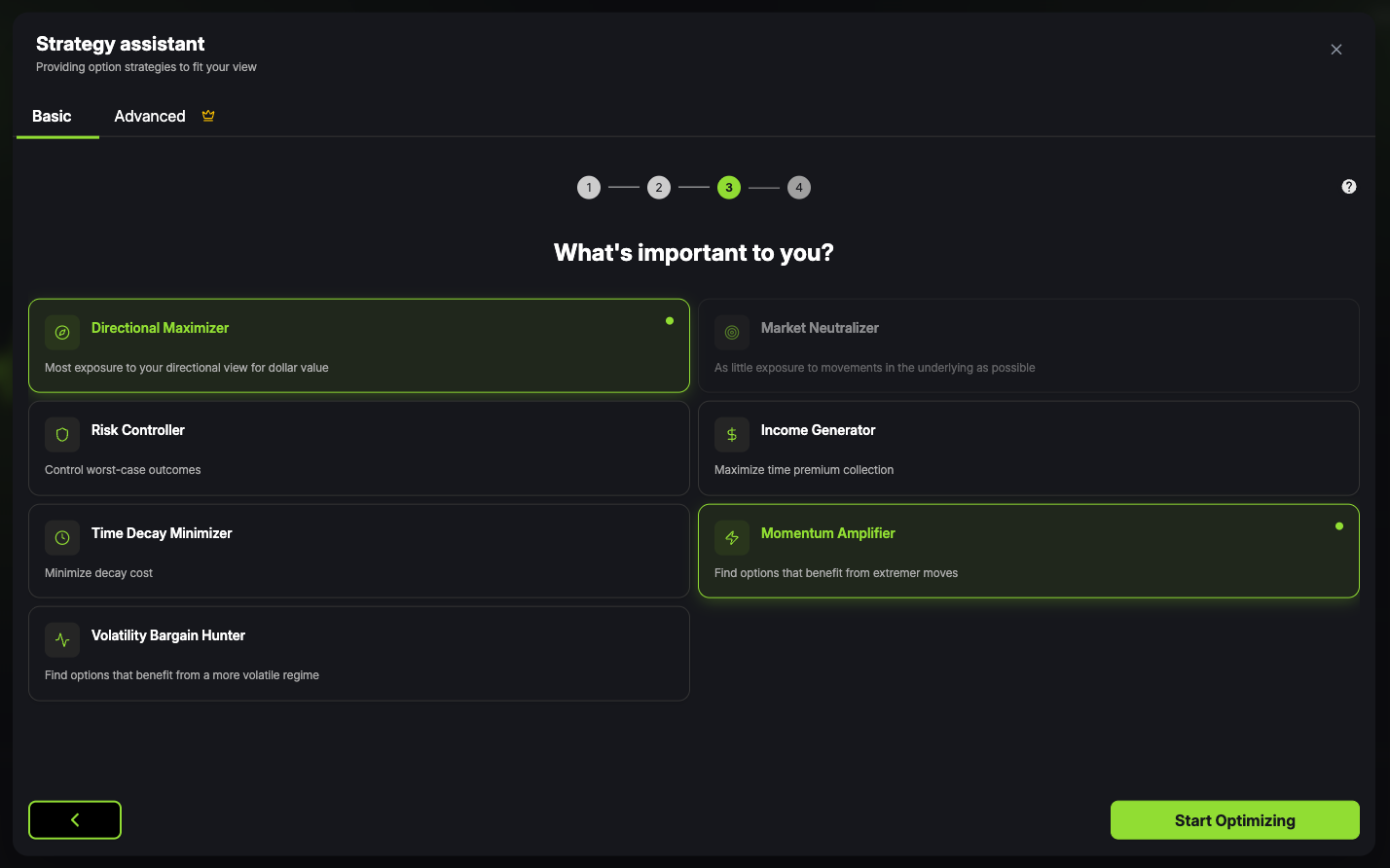

Using it is super easy, as you can simply follow the Strategy Assistant on the Strategy Builder page of OptiView. The wizard takes you through the required steps, where you input the expected move for the underlying, the timeframe and the objectives you want to achieve in plain English. Alternatively, the Plus version of OptiView gives you access to granular controls over objectives and constraints such as the maximum premium to spend, the risk profile, or the number of legs. The Help Centre is a good way to start if you’re unsure how the Strategy Assistant works.

Comparing billions of alternative option strategies to find those that are superior

You've made it this far in this article; OptiStrat must clearly be for you. So let me spill the beans a little on how the algorithm works under the hood and how we managed to level the playing field between professional traders and retail investors.

Optimizing a trade with options comes with three distinct difficulties:

- 1the sheer volume of competing strategies;

- 2a common base on which to compare them;

- 3and a notion for risk in a sphere where losses can exceed the initial investment by a wide margin.

Let me tackle these one by one.

We all know that options only exhibit their full potential if traded in structures, but finding the best combination means evaluating billions of alternatives. A conventional monthly expiration on SPY (the more liquid ETF-alternative to SPX) has one Call and one Put across roughly 200 distinct strikes, which you can either buy or sell. That’s 400 one-legged alternatives, assuming we have a directional thesis for the underlying and can rule out the other half. Allowing for a second leg already lifts that number to 319’600 (we can no longer discard the half with opposite delta). With three legs, you’re faced with more than 85 million alternatives. And with the fourth leg, that number literally explodes to beyond 16 billion. Have fun with your Excel sheet.

The OptiStrat algorithm is based on a high-performance engine built in a low-level programming language ideal for numerical optimization. Paired with clever engineering based on financial intuition (like the fact that two options with the same directional exposure can’t be optimal without an offsetting directional exposure with a domain-splitting strike price), we are able to build the efficient frontier based on live data and user-specific objectives for each request rather than generic and cached results.

How to Compare Option Strategies

The second difficulty is best illustrated by an example. Suppose you intend to gain as much exposure to a move in the underlying as possible. Naturally, a deep in-the-money Call will do the job. However, adding a second Call to the strategy would increase that exposure even further, no?

Well, not so fast. Each additional unit of exposure comes with a real dollar cost. To compare them, we introduce a concept we coin Greek-per-dollar. It essentially answers ‘how much exposure do I actually buy with each 1$?’ and is the dimension we maximize to find the most cost-efficient strategy.

Measuring Risk When Comparing Option Strategies

Lastly, in a similar fashion to maximizing a certain Greek-per-dollar exposure, we obviously want to maximize the investment’s expected return as well. After all, we are doing all this to make money, aren’t we? Unlike a simple stock investment where the return is simply the profit relative to the invested capital, option strategies differ in their risk profile since, for some, there is the theoretical potential for infinite loss, and not all premium-collecting strategies should be considered to return 100%, even when expected to do so under the base assumption.

Let’s look at a little thought experiment where we compare two strategies based on the premise that we expect the underlying stock to increase by 5% over the next 30 days. Buying a Call option below the target price plus the premium would result in a positive expected return. Now, we could artificially “improve” this expected return by reducing the numerator feeding into our expected return equation. Easily done by selling a Put anywhere below our target price. Congratulations, you fooled yourself into an infinite expected return.

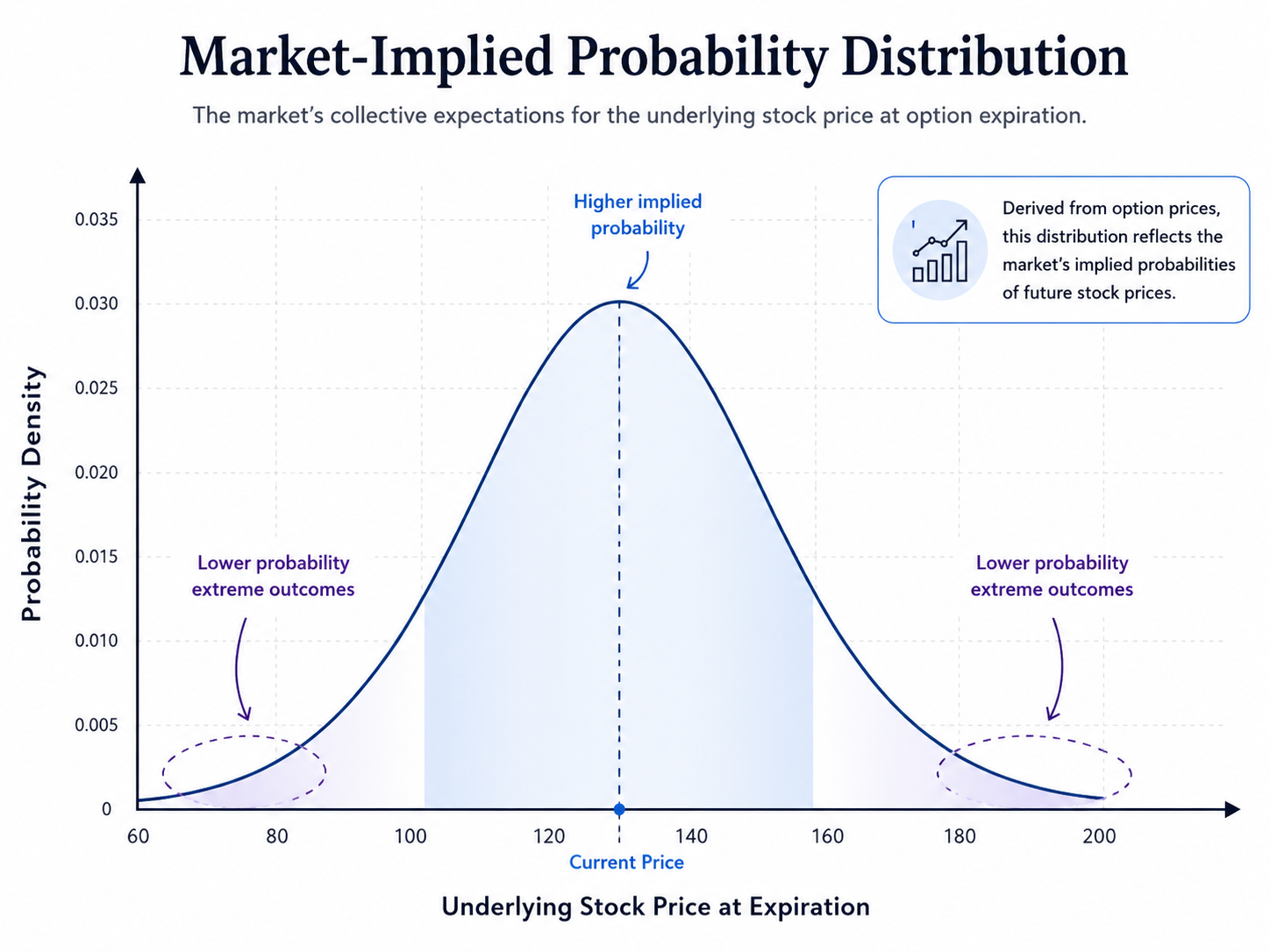

So, let’s talk about risk. Easy to spot why expected return doesn’t always equal expected return in options trading. The finite risk of a single long Call is clearly less risky than the potential loss the naked short Put leg entails if the expected move in the underlying does not materialize. To establish a common notion for risk, the OptiStrat algorithm uses the 90%-cVaR (adjustable to 5% and 20% under the Plus-plan) of a strategy to scale its expected payoff when searching for the strategy with the highest (risk-adjusted) expected return.

Conditional Value at Risk (cVaR) is itself an expected value of potential loss. Precisely, it corresponds to the average loss in the 10% (= 100% - 90%) of the worst outcomes under market-implied probabilities. And here’s what sets OptiStrat truly apart from anything available to retail (and even most non-option-focused hedge funds). Instead of relying on the simple max loss or vaguely approximated capital-at-risk replacements, the algorithm extracts the market-implied distribution for the underlying’s stock from the options surface in real time, computes the expected loss if the worst 10% materialize, and finds the trade that is truly efficient.

The Easiest Way to Find the Best Option Strategy – Manual Strategy Selection vs OptiStrat

| Manual Analysis | OptiStrat |

|---|---|

| Reviews a handful of strategies | Compares thousands simultaneously |

| Hours of analysis | Seconds |

| Subjective decisions | Quantitative ranking |

| Overlooked alternatives | Exhaustive search |

| Requires advanced domain-knowledge | Suited for all investors due to guided workflow |

The right tool to identify the best options trade

Balancing the trade-offs in different option strategies has always been a hopeless endeavor without sophisticated tools and in-depth domain knowledge. While a handful of competing options may be compared manually, a normal option chain offers millions of alternative structures.

A better approach than randomly picking a strategy and trying to fit it to a narrative is to start with the assumptions themselves and let the data determine the most efficient way to trade. OptiStrat allows you to define your assumptions, specify your objectives and constraints in plain English, and search all possible combinations exhaustively live to find the optimal trade setup for you.

Give it a try and see what strategy best fits your market view.