'/%3e%3c/svg%3e)

'/%3e%3c/svg%3e)

Scan the options market with these four simple filters for better option trade opportunities

Finding the right options contracts can be challenging. In this article, we explore key metrics to help you identify better trade opportunities and cut through the noise.

With around 60 million options contracts traded daily in the U.S., finding high-quality opportunities can feel like hunting for a needle in a haystack.

In a previous article on OptiScan, we showed how the Option Scanner helps traders cut through the noise by filtering the entire options universe based on their own criteria. But what if you don't yet know what those criteria should be?

This article breaks down a set of foundational filters to help options buyers quickly narrow the field and focus on what matters.

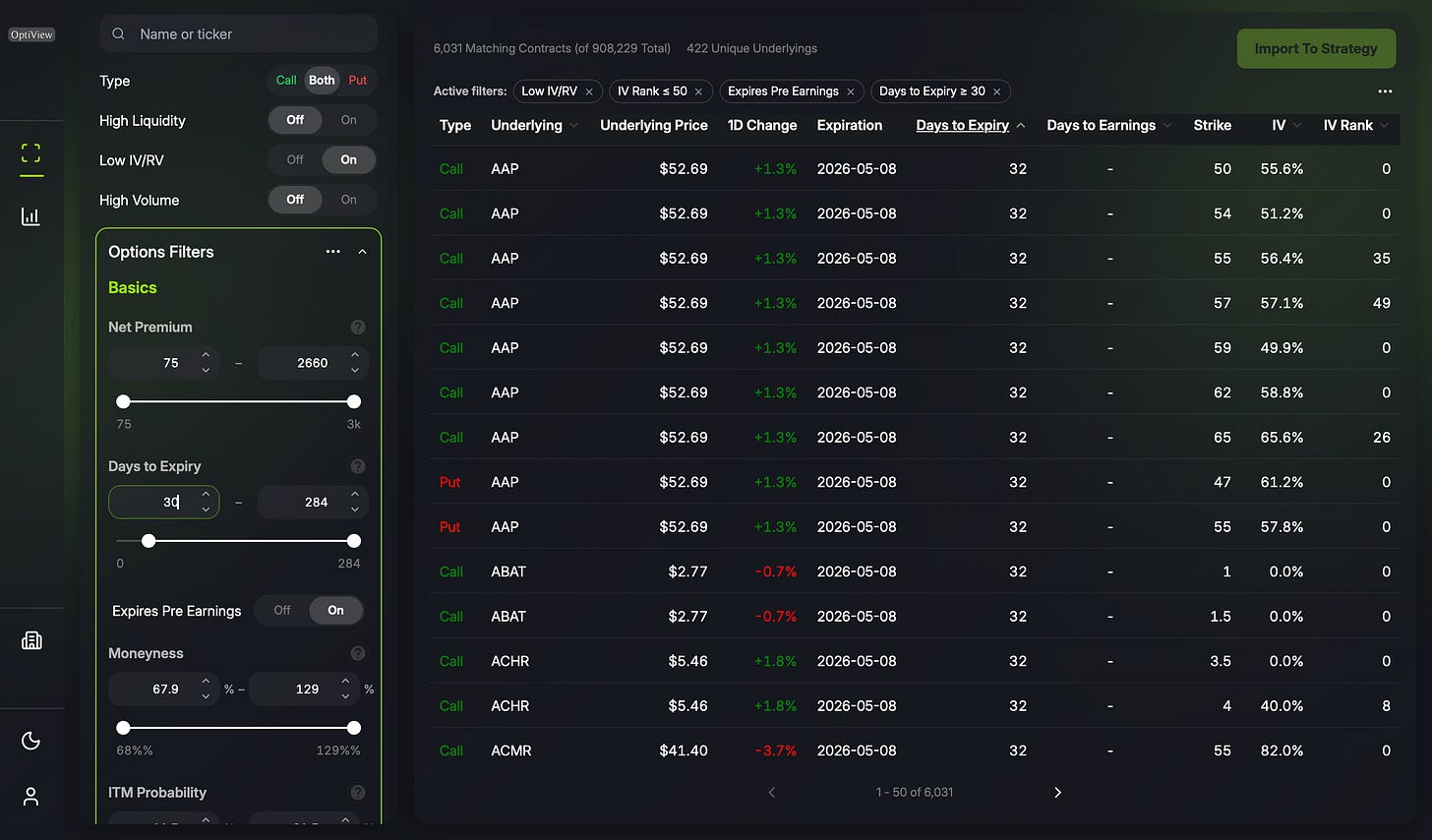

Implied Volatility

You've heard it before and you'll hear it again: implied volatility (IV) plays a critical role in how an options strategy performs. Identifying when IV is relatively low can significantly improve trade entry.

But how do you know when IV is "cheap"?

Two useful indicators are:

- Low IV rank

- IV below realized volatility

Together, these help determine whether options are priced below both their historical norms and actual realized market movement. When that happens, it may signal attractive entry opportunities.

An easy way to do this is by applying an IV rank filter to the options universe, or switching on a low IV/RV toggle in the Option Scanner to instantly eliminate trades that don't match this criteria.

In addition, you can find additional analytics on your selected option's IV profile in the multi-functional panel of the strategy builder.

Pre-Earnings

Another valuable filter is identifying options that expire before earnings announcements.

As covered in our article on IV crush, implied volatility tends to rise ahead of major events, like earnings, driving up option premiums. Once the event passes, that uncertainty collapses, often leading to a sharp drop in IV and premiums.

By focusing on options that expire before earnings, traders can potentially avoid this volatility crush. Even more effective is targeting longer-dated options i.e. those with at least 30 days until earnings, while still expiring before the event. These tend to have less inflated IV compared to near-term contracts, where anticipation is already priced in.

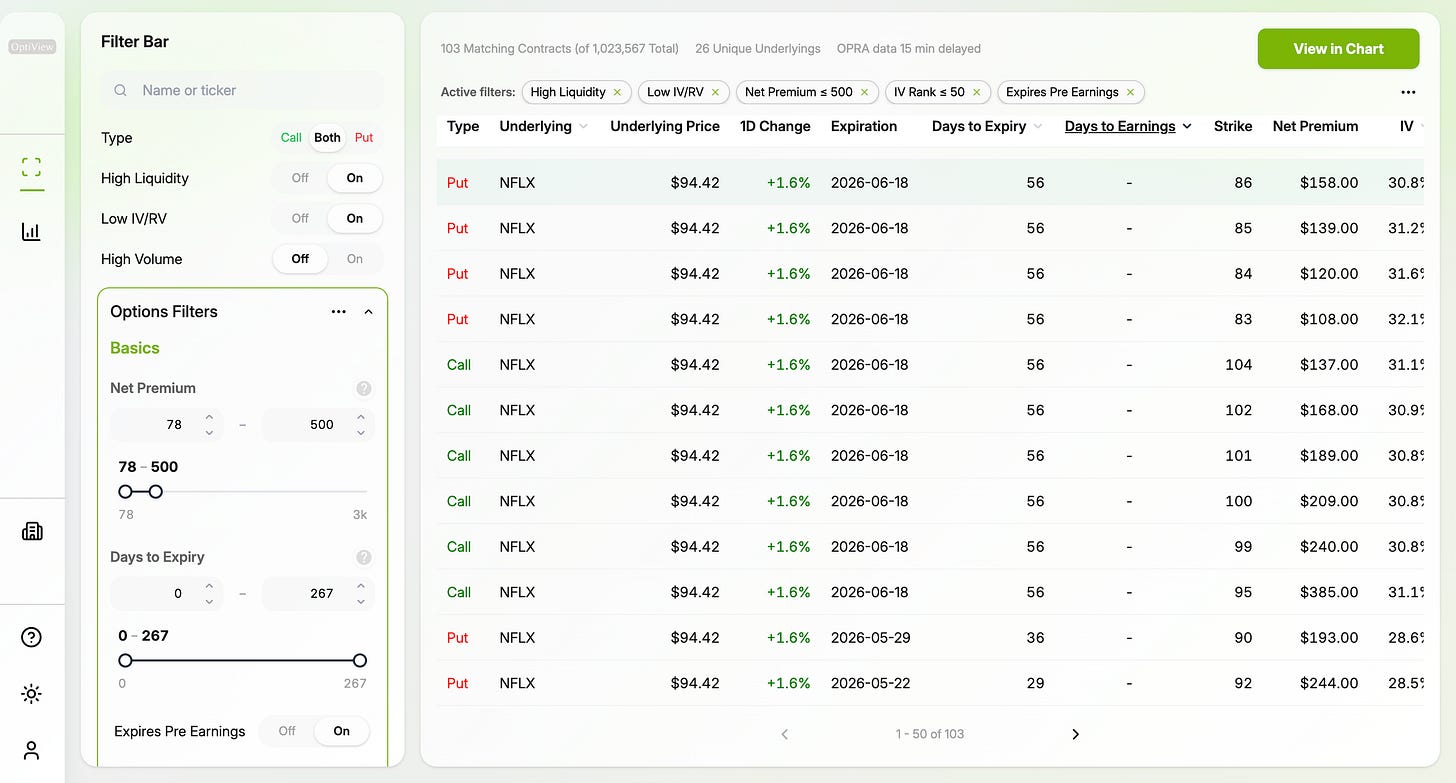

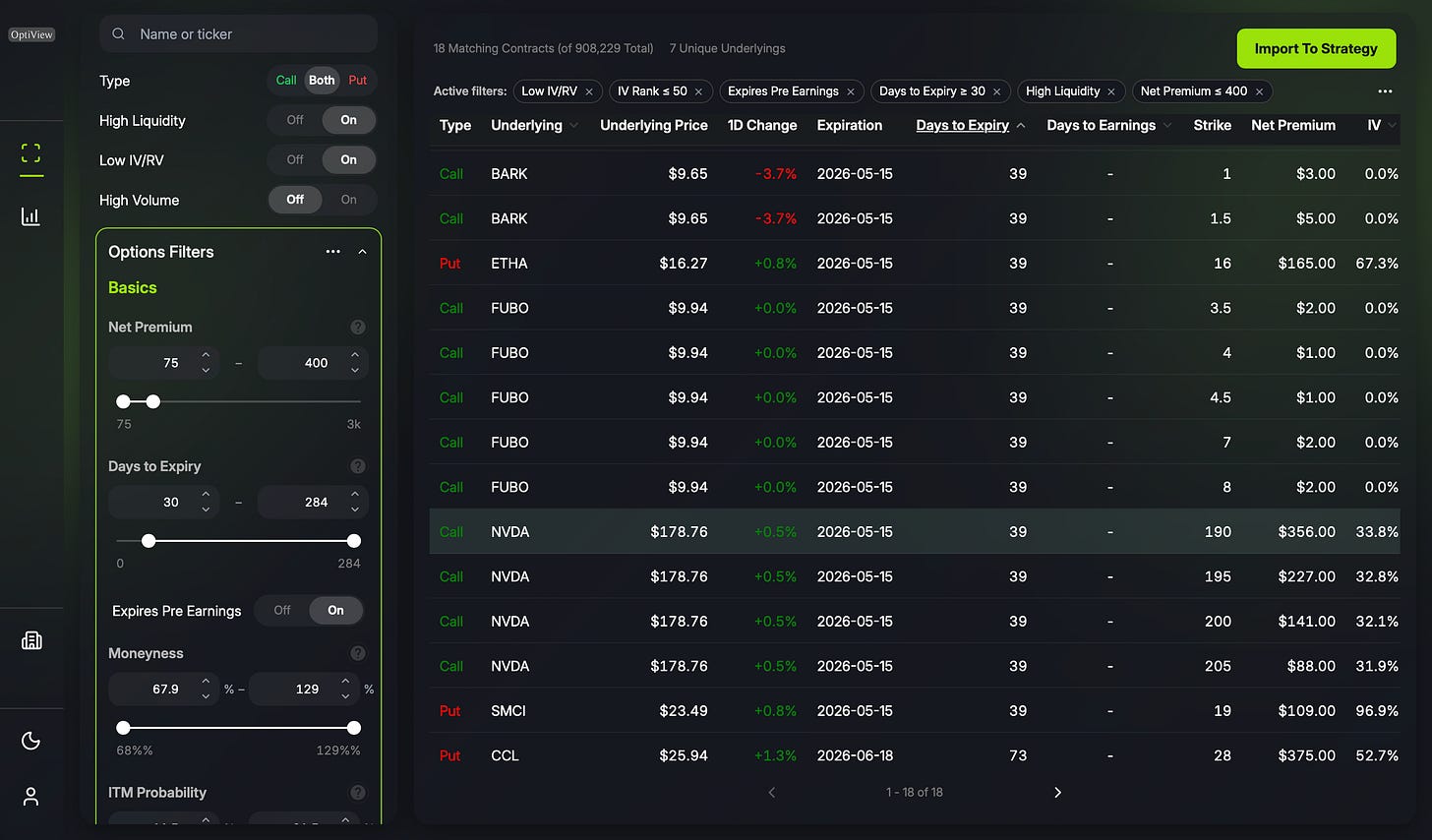

High Liquidity

Liquidity is a critical filter, especially for traders sensitive to pricing and execution.

Lower premium options often include:

- Illiquid contracts

- Deep out-of-the-money options

- Near-term expirations

These frequently come with low volume and wide bid-ask spreads, making exits more difficult. Filtering for high liquidity, such as tight bid-ask spreads (e.g. under 3%) and strong open interest, helps ensure smoother execution and more reliable pricing.

Net Premium

Finally, net premium is a key consideration, particularly for retail traders.

With standard contract sizes of 100 shares, premiums can quickly scale into the thousands, making position sizing a real constraint. Filtering by net premium allows traders to align opportunities with their available capital and risk tolerance from the outset.

It also helps enforce discipline. By setting clear premium thresholds, traders can avoid over-allocating capital to a single position and maintain a more balanced portfolio.

Of course, this article is not exhaustive. There are many other worthwhile checks and filters you can apply to the options universe depending on your trading strategy and criteria for entrance.

OptiView offers a wide range of fundamental and technical filters on both underlyings and options, which can be accessed for free in the Option Scanner. Happy trading!