'/%3e%3c/svg%3e)

'/%3e%3c/svg%3e)

Options and global uncertainty: A path to profit in turbulent markets

How to turn uncertainty about the future into strategic opportunity and align your investments in an era of high volatility.

Well, it looks like the volatility we observed in 2025 is here to stay in 2026 as well. With the current U.S. administration still in office for another three years, persistent uncertainty around the future of AI, and geopolitical tensions heating up (or outright combusting) in the Middle East and Eastern Europe, we can likely expect another wild ride in the years ahead.

Yet, traditional stock markets recoil at any whiff of uncertainty, and the effects for short and medium-term traders are particularly pronounced, with sudden portfolio drops hurting.

In this article, we explore how you can strategically position yourself in the options market by deliberately trading volatility. In particular, we cover:

- How to compose straddles and strangles as volatility plays

- The difference between macro and event-driven volatility

- Why its important to know which one you're playing (if not, both)

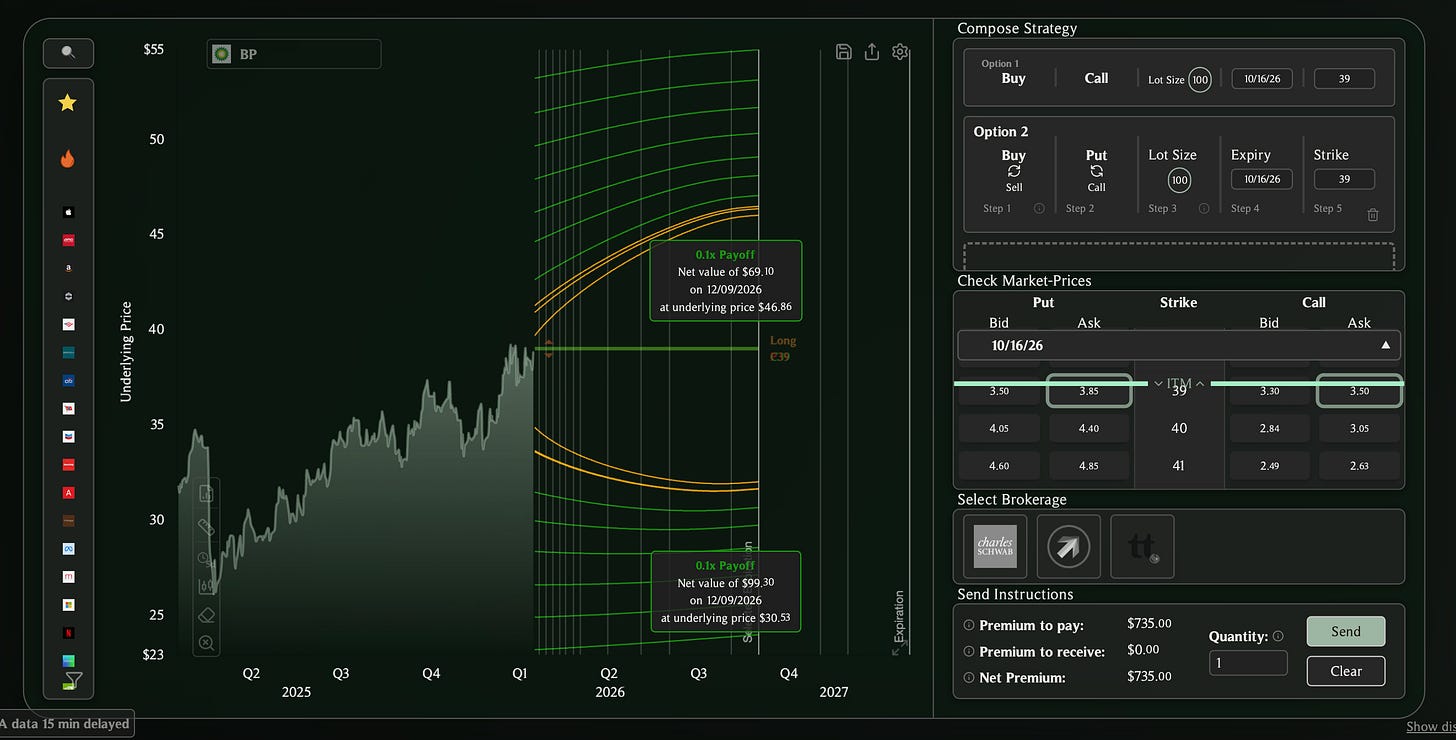

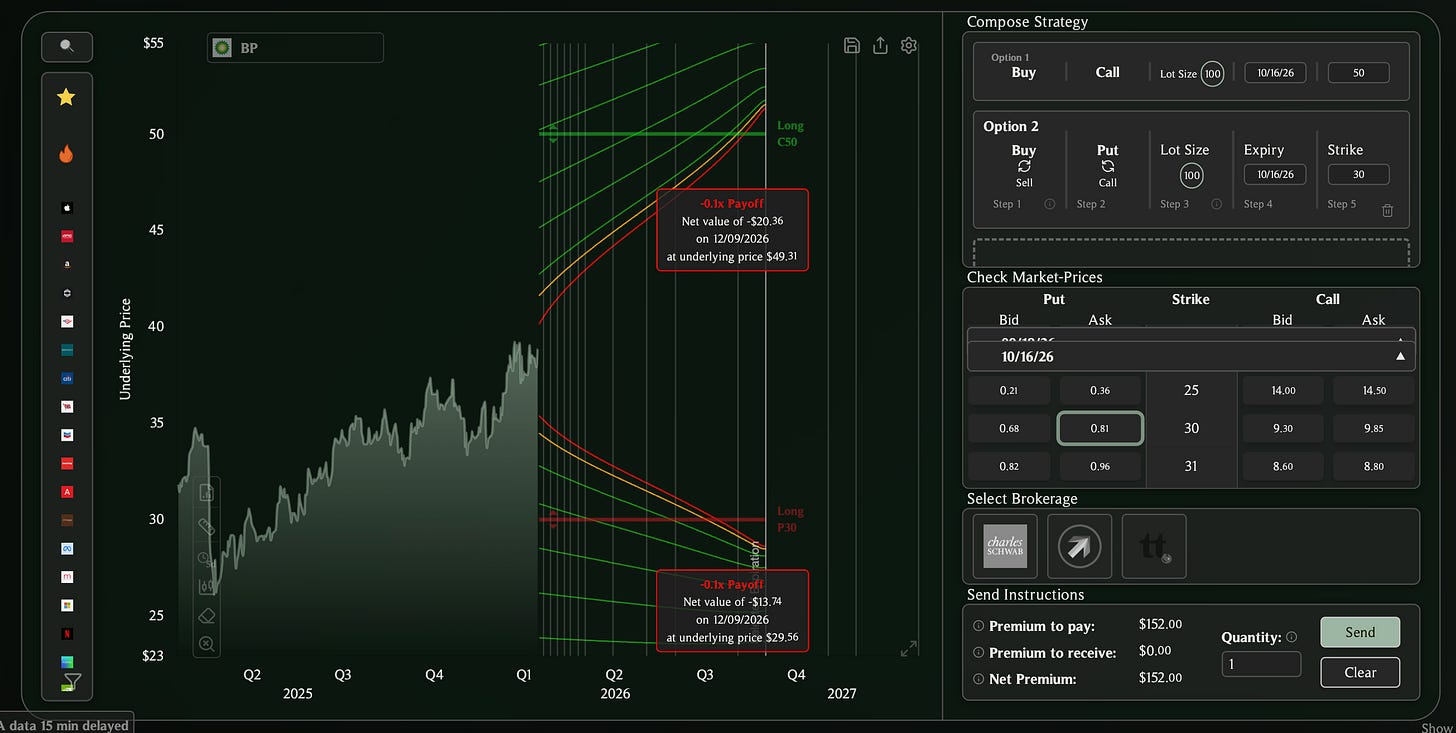

Straddle & Strangle Strategies

Two common options strategies known as volatility plays are the straddle and the strangle. In both strategies, an investor simultaneously purchases a call and a put option, typically with the same expiration date. From a payoff perspective, the holder benefits from price movements in either direction, upward or downward, in the underlying asset.

The worst-case scenario for both strategies occurs when the underlying asset remains relatively stable or does not exceed the movement required to generate positive payoffs. In that case, both options expire worthless, resulting in a total loss equal to the combined premiums paid for the call and put.

So what distinguishes a straddle from a strangle? The key difference lies in how far out-of-the-money (OTM) the options are at initiation. In a straddle, both the call and put are typically purchased at-the-money (ATM). This requires a higher upfront investment (higher total premium) but also increases the likelihood of profitability since the underlying does not need to move as far for the position to break even.

In contrast, a strangle involves buying a call and a put that are further out-of-the-money, often at different strike prices. This lowers the initial cost (lower total premium), but the underlying asset must make a larger price move for the strategy to become profitable, reducing the probability of payoff.

Nevertheless, in both cases, the payoff profiles are strongly aligned towards yielding in volatile markets.

You can build a straddle or strangle on OptiView in the Strategy Builder.

General volatility vs. event driven volatility

Before trading a straddle or strangle, it is important to understand how different types of volatility might impact payoff dynamics. Broadly speaking, we can distinguish between general macro volatility and event-driven volatility.

General macro volatility refers to periods of heightened uncertainty or turbulence across financial markets, such as during recessions, pandemics, or geo-political instability. In these situations, periods of elevated implied volatility (IV) are often observed. When IV remains relatively stable at higher levels, entering a straddle or strangle position depends primarily on realized price movements - what's referred to as a gamma play. In this context, the strategy's value may be largely driven by significant price swings in the underlying asset, rather than uncertainty driven by anticipation of a specific event (IV).

Event-driven volatility, on the other hand, arises from specific, highly anticipated events such as Federal Reserve announcements, elections, earnings releases, or regulatory decisions. In these situations, the relative importance of vega and gamma shifts over time. As discussed in our previous article on volatility compression, implied volatility tends to increase in anticipation of a major event and then drop sharply once the event has occurred and uncertainty is resolved. This post-event decline in IV, often referred to as IV crush, typically leads to a decrease in option values, as the market is no longer willing to pay as much for optionality.

After this volatility compression, holding a straddle or strangle becomes more of a gamma-driven position, where the strategy's value depends primarily on the magnitude of price movements in the underlying asset. If you believe that the post-event price swings will outweigh the negative impact of the IV crush, maintaining the position may be justified.

Why identifying the volatility cycle matters

It is entirely possible to trade both macro and event-driven volatility simultaneously. In fact, periods of macro volatility often set the stage for increased event-driven volatility. For example, sustained geopolitical tensions can lead to a greater frequency (or anticipation) of market-moving developments, such as sanctions announcements, defensive escalations, Fed policy decisions and CPI releases.

Most importantly, however, traders should ensure that the duration of their trade aligns with their broader thesis on how volatility is likely to unfold. Understanding which phase of the volatility cycle you are betting on is critical to structuring the position appropriately and managing position entry and exit strategy dynamics effectively.

Once you identified a pattern and built conviction around your belief, you can have our Strategy Assistant help you identify high-potential trades that match your constraints and objectives.

Of course, this article is not intended to provide an exhaustive list of options strategies for periods of heightened volatility. Rather, our goal is to demonstrate how to structure volatility-driven trades to capitalize on global uncertainty, while highlighting the key considerations for both entry and exit.

We hope you found this article insightful and valuable and let us know what you'd like to read next!