'/%3e%3c/svg%3e)

'/%3e%3c/svg%3e)

The volatility compression killer, and how it can ruin your options strategy.

Why Implied Volatility (IV) matters—and how to use it to find better options trades

When Being Right Isn't Enough

Options are a unique asset in the sense that one must not be merely right about the underlying's direction. All too often, retail investors are caught by surprise when they end up losing premium value despite their underlying thesis of stock movement being correct. The fact is, the value of an option is inherently linked to key forces which every options investor should be aware of:

- Intrinsic Value: For example, determined by the options type, strike price & price of the underlying at any given point, and;

- Extrinsic Value (aka Time Value): Determined by both the option's proximity to expiration and implied volatility. Whilst many understand the role of time-decay in an options value, the role of implied volatility seems to be one that is rather misjudged by beginner traders.

Implied Volatility (or IV) is a baked-in component in an options price that reflects the market's expectations of volatility in the underlying stock. It differs from Realized Volatility (or RV), as it is implied, meaning it is a market-driven expectation or forecast that has not yet been observed. For example, a high IV indicates there is significant uncertainty surrounding future price movements. Despite its heavy reliance on market sentiment, IV plays one of the most significant roles in determining how your options strategy plays out; either making it or breaking it.

The Quiet Damage of Volatility Compression

Volatility compression happens when your option's IV decreases after you've entered a trade. In practical terms, it means the market has reassessed future uncertainty and no longer expects price movements to be as extreme as previously anticipated. Consequently, the option's value falls as the premium investors are willing to pay for uncertainty is reduced. Sometimes this can happen unexpectedly, but many times IV compression is associated with the aftermath of earnings announcements or large corporate announcements like regulatory decisions, M&A, clinical trials and/or court rulings. In any case, timing matters. Entering an options trade without accounting for potential IV compression can quietly erode value, even if the underlying moves in the anticipated direction.

Finding Opportunity Where Volatility Is Misunderstood

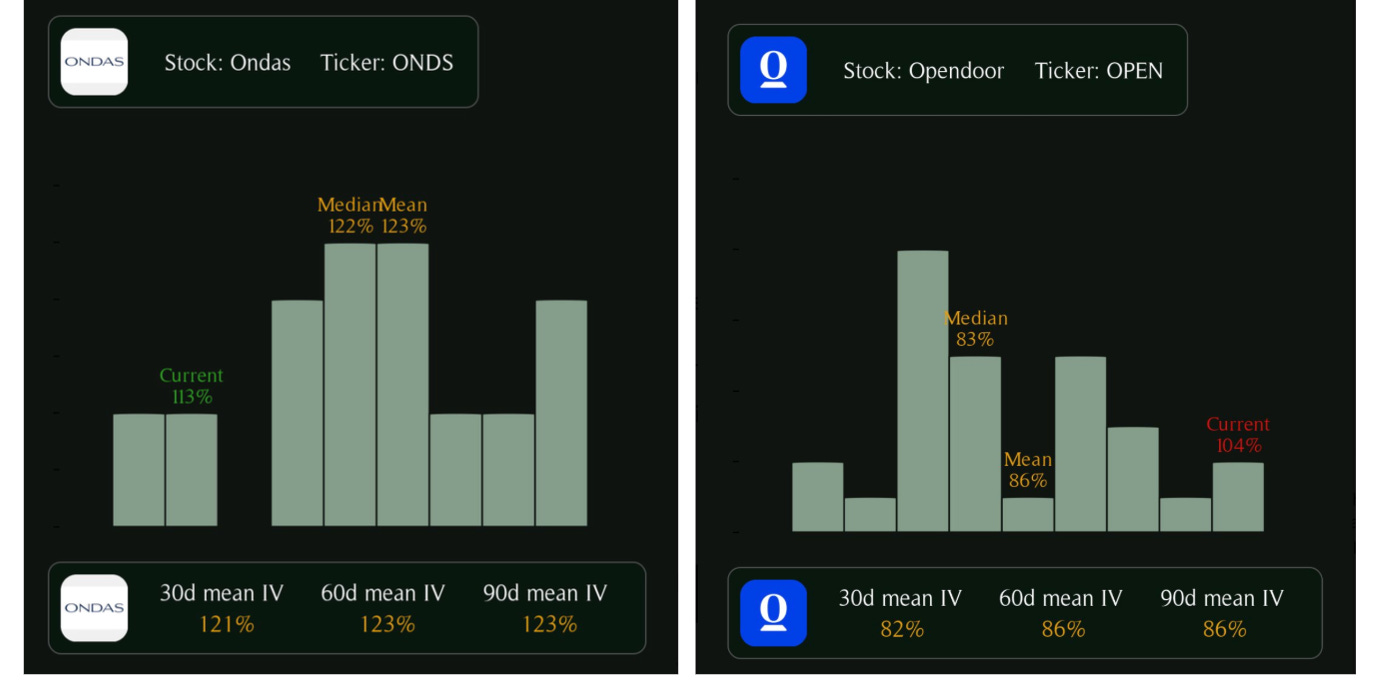

It's not all doom and gloom. In fact, by knowing how IV impacts an option's price, it's one of the key ways in which you can recognise and take advantage of potential market mispricing. For example, an option which is trading below its mean IV might offer a unique opportunity to purchase whilst the premium component which prices in IV remains low, subsequently enjoying an increase as the IV converges closer to its mean later on.

On the flip side, an option which is trading with IV higher than the mean may not only pose a warning to option buyers to hold off, but might indicate a lucrative opportunity for option sellers. Sellers benefit directly from volatility compression, as a decline in IV reduces the value of the options they've sold, allowing them to repurchase those contracts at a lower price or let them expire worthless.

Importantly, it helps to have the right tools at your hand when evaluating this relationship between current and mean IV. Tools such as OptiView let you see the historical IV and its distribution for individual contracts and whole option combinations in the extendable panel below the main chart. With this feature, it becomes easy to quickly evaluate options and spot potential opportunities.