'/%3e%3c/svg%3e)

'/%3e%3c/svg%3e)

The Options Market in 2025: We've read the data so you don't have to.

The 2025 CBOE Review of the Options Industry is out! We'll take a look at some of the key trends and themes emerging from the options market.

2025 was a year of big dreams and high hopes. Marked by significant market volatility driven by tariffs, geopolitical uncertainty, and corporate wins and blunders, the opportunities for options traders were boundless. Once again, trading volume reached a new all-time high, coming as no surprise to those who have been closely following the development of the market. While pre-existing retail trends such as 0DTE, ETF and single-stock options continued to prevail, we also highlight several notable surprises from the most recent 2025 CBOE Options Market Year in Review report.

Continuing trends

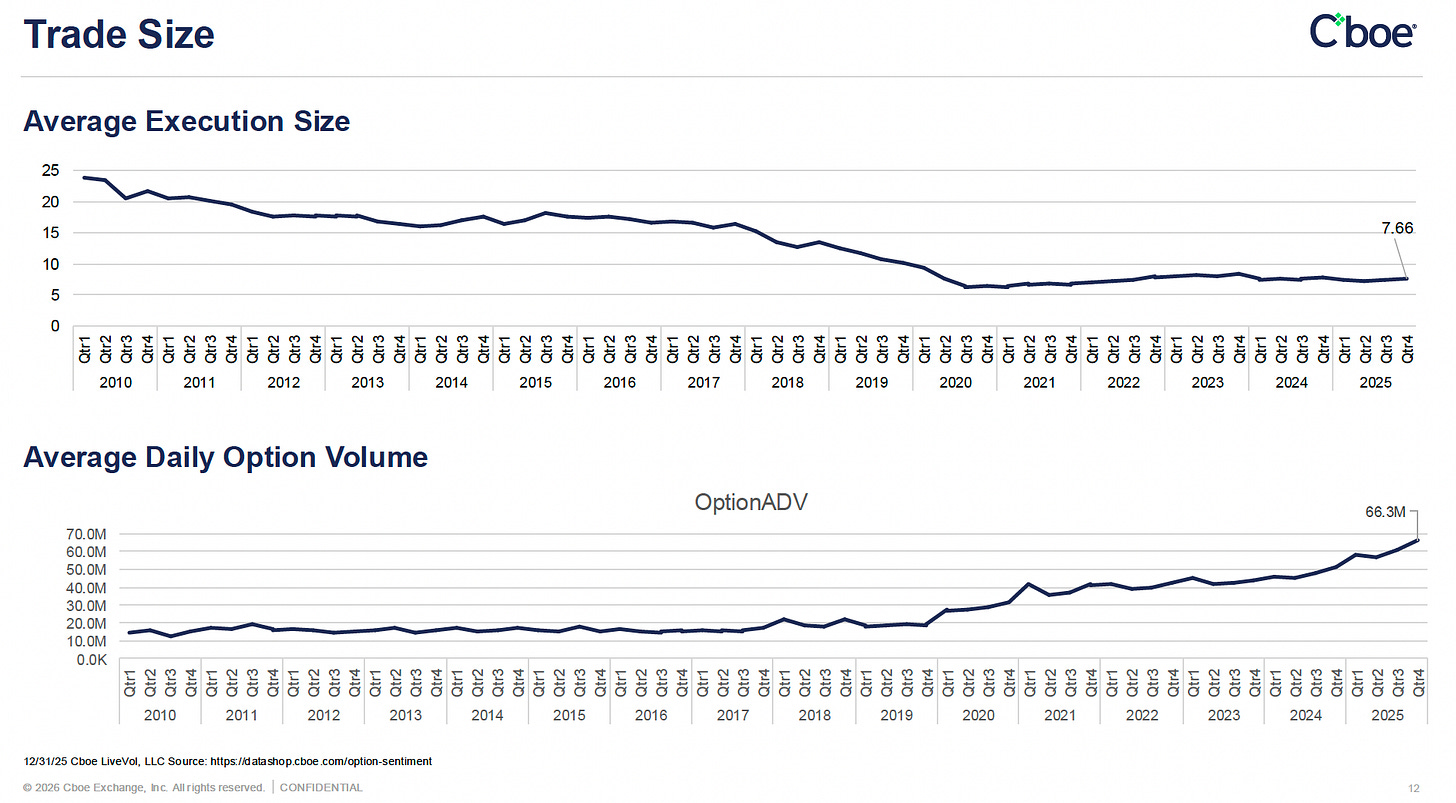

Retail-Driven Shifts in Execution Size and Volume

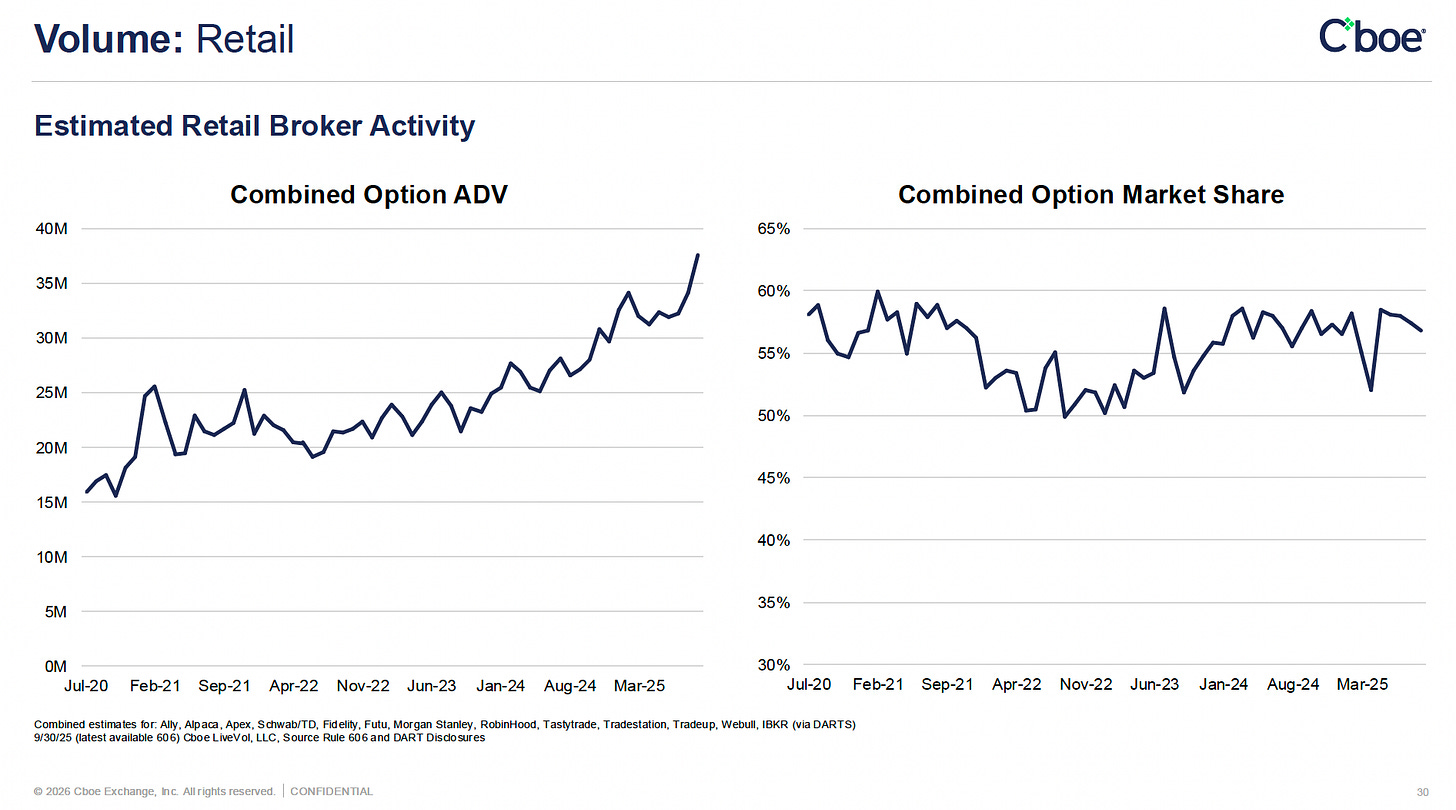

Let's first look at trends that have continued to firm up over time. We begin with the sustained increase in options trading volume alongside the rise of the retail trader, who now accounts for approximately 50% of total volume. At the same time, we've observed a considerable decline in average execution size paired with a significant increase in overall options volume, reaching roughly 66.3 million contracts in Q4 2025, compared with 15 million contracts in Q4 2010. What was once an institutionally dominated market characterized by large execution sizes now shows average trade sizes at roughly one-third of their 2010 levels. This shift is not surprising, as retail trading is typically defined by smaller trade sizes than those of institutional participants, who often transact in larger sizes to hedge risk and have greater capital at their disposal.

Product Concentration

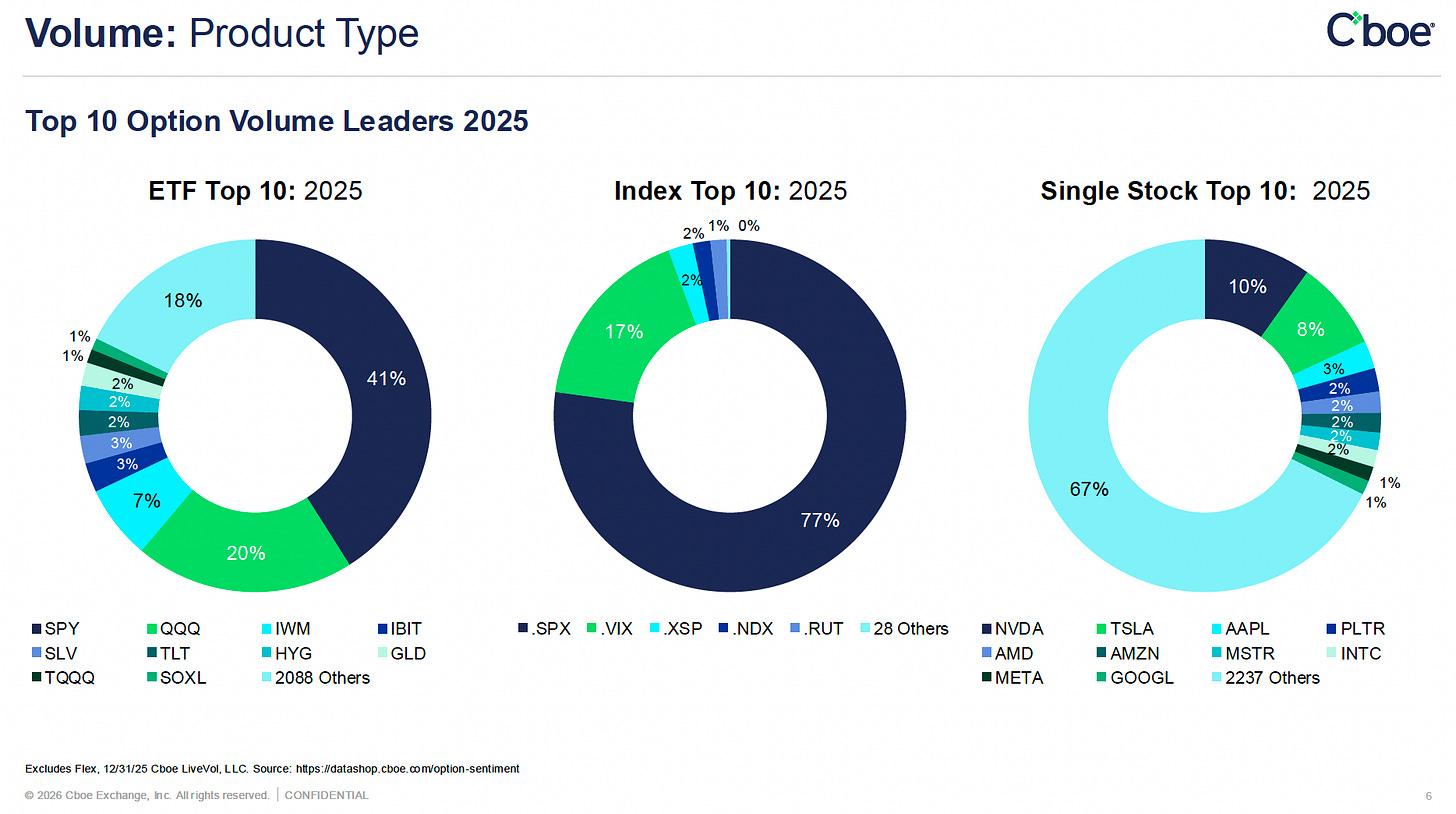

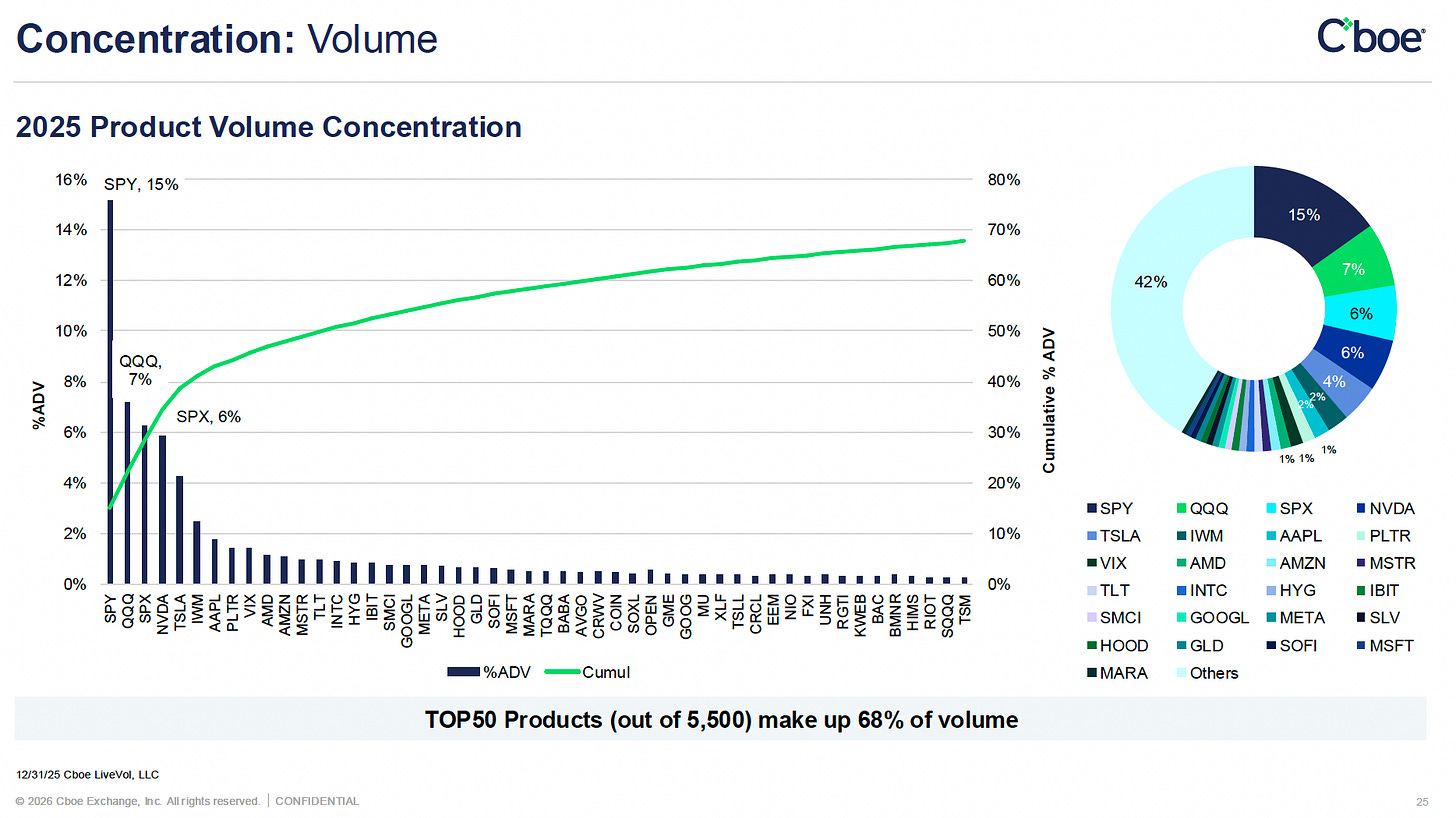

The year 2025 was no exception when it came to product concentration. The top 50 options products accounted for 68% of total trading volume and 85% of total premium. By product class, single-stock options remained the most heavily traded, followed by ETF options and then index options. Within single-stock options, Nvidia led activity, accounting for 10% of volume, followed by Tesla at 8%. In index options, SPX dominated, representing a substantial 77% of total index options volume. For ETF options, SPY accounted for 41% of volume, with QQQ and IWM following at 20% and 18%, respectively. Looking across all individual products, options trading remains heavily concentrated in a small number of ETFs, particularly SPY and QQQ, highlighting their position as the most actively traded options products overall.

Short-Dated vs. Long-Dated Options

Short-dated options continued to prevail over long-dated options in 2025. This trend has been evident since 2022, when contracts with less than one week to expiration first surpassed those with longer durations. Since then, growth in short-dated options has increasingly outpaced that of long-dated contracts, with the gap widening further in 2025. In addition, 0DTE options volume has grown YOY by 41% since 2020. The continued expansion of short-dated options trading is once again likely driven by retail participation, which tends to favor strategies that deliver quicker outcomes.

Emerging trends

Rise of FLEX Options

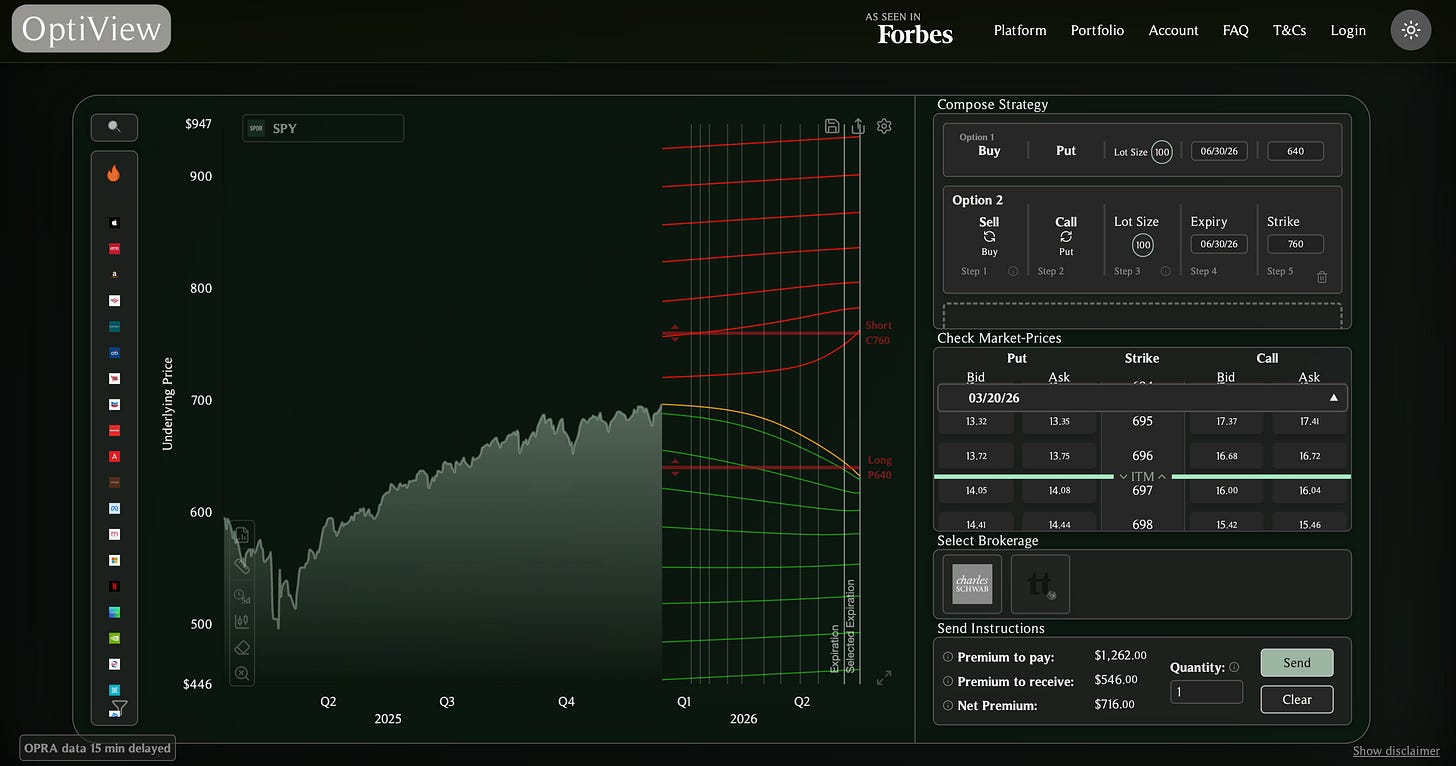

One notable development is the rise of FLEX options, which have experienced tenfold growth since 2019. Average daily volume has increased from approximately 150,000 contracts in 2019 to 1.3 million in 2025, suggesting that FLEX options are here to stay. Primarily traded on single-stock and ETF options, FLEX options are customized contracts that allow investors to tailor key contractual terms. As exchange-listed instruments, they benefit from standard clearing processes that reduce third-party risk, while still offering a level of customization similar to OTC options. FLEX options trade via a Request for Quote (RFQ) system, as there is no continuous quote stream. This growing product class has attracted particular interest from institutional participants, as FLEX options are a core component of defined-outcome ETFs that employ options strategies to deliver a predetermined range of yields over a set time horizon.

Assuming ownership of the underlying (SPY for example), you can construct a similar defined outcome strategy in OptiView by selling a 10% OTM call and buying a 10% OTM put. This collar structure caps upside while providing downside protection, allowing investors to hedge equity risk in exchange for more stable, predictable return profiles. No fees are charged in OptiView.

Heavier Retail Investment

While trends in volume and execution size can largely be attributed to growing retail participation in the options market, a closer look at retail activity reveals an additional insight. Although retail market share has remained relatively stable (fluctuating between 50% and 60%), average daily options volume has increased steadily since 2020, rising from approximately 15 million contracts to 37 million in 2025. This suggests that the existing retail participant base is not necessarily expanding, but rather that current participants are trading options more heavily. Given the complexity of options as an asset class, particularly for retail investors, it is unsurprising that market participation itself has plateaued. Instead, those who have already navigated the steep learning curve appear to be increasing their engagement and continuing to capture the benefits of options trading.

Regulatory Shifts and Brokerage Offerings

Last but not least, regulatory developments suggest growing momentum toward a more flexible application of FINRA's Pattern Day Trading (PDT) rules, which could materially expand market participation by lowering barriers for smaller accounts and driving increased retail accessibility to options trading. At the same time, brokerage platforms are strategically broadening their product suites to capture this demand, with a particular focus on expanding access to options and emerging prediction markets. The rapid adoption of prediction markets reflects rising investor interest in alternative instruments that offer event-driven exposure and diversification beyond traditional equities. Collectively, these trends signal a more inclusive and innovation-driven trading environment, with potential tailwinds for brokerages positioned to scale access while maintaining effective risk management.

And that's a wrap for 2025. Let's see how the next year develops for the options market; I have a feeling it's going to be a good one. Make sure to subscribe if you want to follow our articles for the year ahead.