The leading platform for options analytics and trading

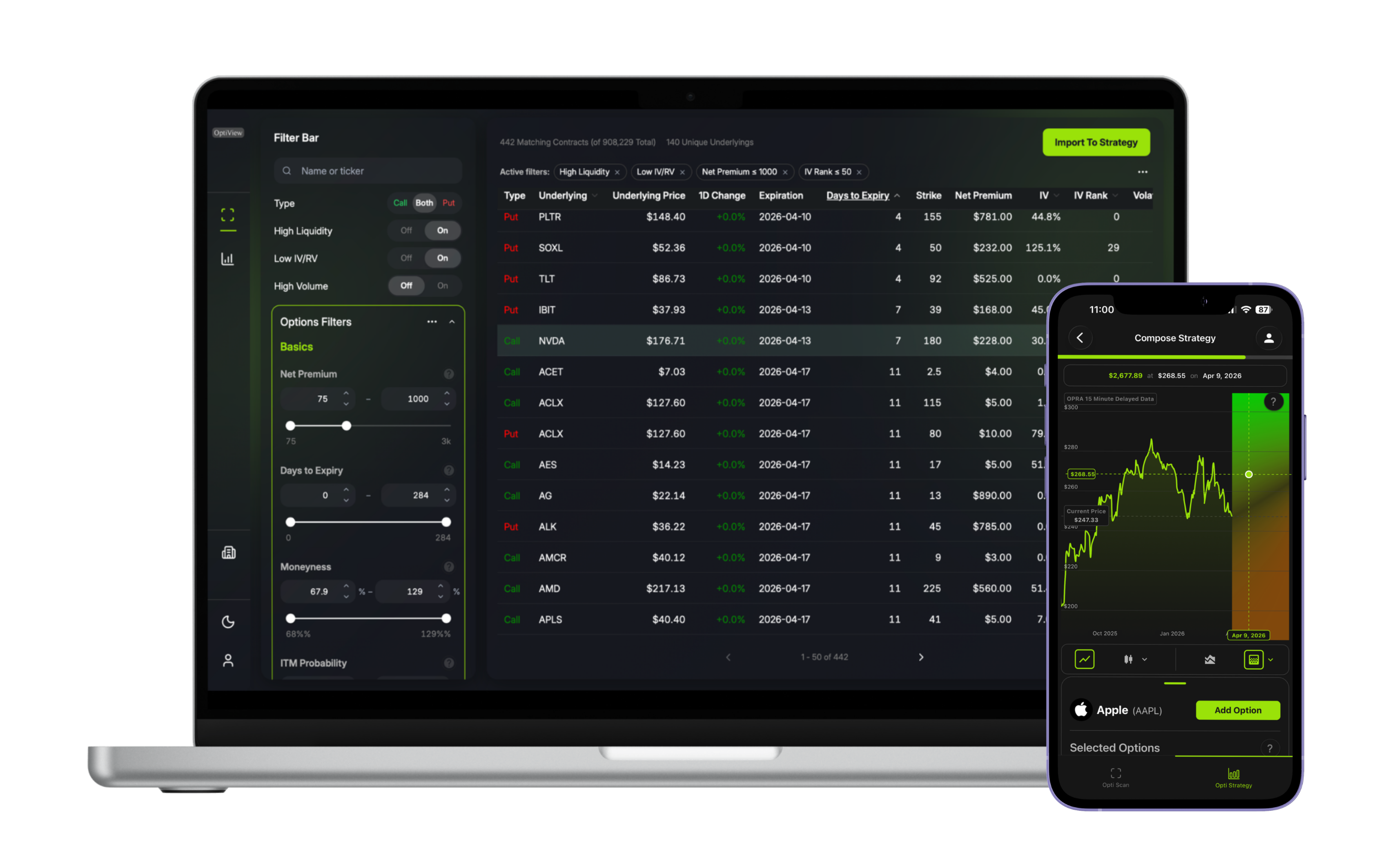

Find the right options at the right time with OptiView Desktop and Mobile apps

Integrated with major U.S. brokers

Connect your brokerage account to access live U.S. equity and options data and order execution capabilities. Alternatively, use OptiView’s free 15-minute delayed OPRA data feed, no broker connection needed.

What we offer

OptiView gives you advanced tools to find high-performance trades and stress-test your P&L with confidence.

Scan the universe

Filter the entire universe of U.S. listed options with OptiScan to surface high-potential trades instantly.

Payoff Visualization

Explore full P&L outcomes for single- and multi-leg strategies through expiration in our OptiView chart.

Free options data

Access a rich pool of historical, 15-minutes delayed and live* options data.

Optimize your strategy

Algorithmically find optimized alternatives that maximize efficiency and outcomes.

Stress-test positions

See how your strategy performs under different volatility regimes, dividend yields, and interest rates with our stress testing feature.

Gain access to trade insights

Join our network to keep up to date with global trends and receive the latest on trade insights, idea generation, strategies and more.

Keeping you safe

Online security is always a priority. We implement a range of controls to keep your data and account safe.

Brokerage authorization

Connect to your brokerage account using industry standard OAuth2.0. We never see your brokerage credentials or login details.

Data encryption

We keep your personal data from your OptiView account fully encrypted in transit and at rest.

Data confidentiality

We adhere to all relevant data rules including EU GDPR requirements. Find out more in our privacy policy.

Direct support

We provide direct and responsive support for any issues with your account at [email protected].

Payment

Take advantage of our free plan or upgrade to premium for access to even more advanced analytics

Free Plan

Access options data and OptiView’s core tools for free, no commitment required.

$0 / monthFree forever

- Free options data

- Option universe scanner

- Strategy builder

- Payoff visualization

- Strategy optimization

Premium Plan

Gain access to additional features and advanced analytical tools.

$20 / monthBilled $20/mo

- Deep Search strategy optimization*

- Trade discovery under asymmetric risk*

- Stress-testing panel*

- Full IV profile view*

- Unlimited strategy tabs

Frequently Asked Questions

Everything you need to know about OptiView and options analytics.

Explore the next-gen in options trading today

Available on desktop or you can download our app on the App Store or Google Play store.